In the late 1990’s, early in my career managing mutual funds with my mentor Dr. Martin Zweig, we would get on a weekly call with Advisors who had clients in our funds to answer questions about the markets and what Marty was thinking. Invariably someone would ask, “What about gold, Marty”? Gold peaked in September of 1980 at just under $700 an ounce and didn’t sniff that level again until 2007, when it broke out as commodities rallied broadly in the mid-aught years until the financial crisis on 2008-09 sunk other industrial commodities, such as copper, while gold continued its trek higher. I always got a chuckle at that question, as most of my career up to that point gold was a terrible investment, and these “gold bugs” struck me as old time advisors fighting the inflation battle that Paul Volker and the Fed had won nearly 20 years earlier. Basically gold went nowhere between the mid-80’s and mid-2000’s, in a period of time when bonds were a great investment, and even with a couple brutal bear markets, stocks did incredibly as well. Adjusted for inflation, gold was a particularly bad investment in the 1980-90’s.

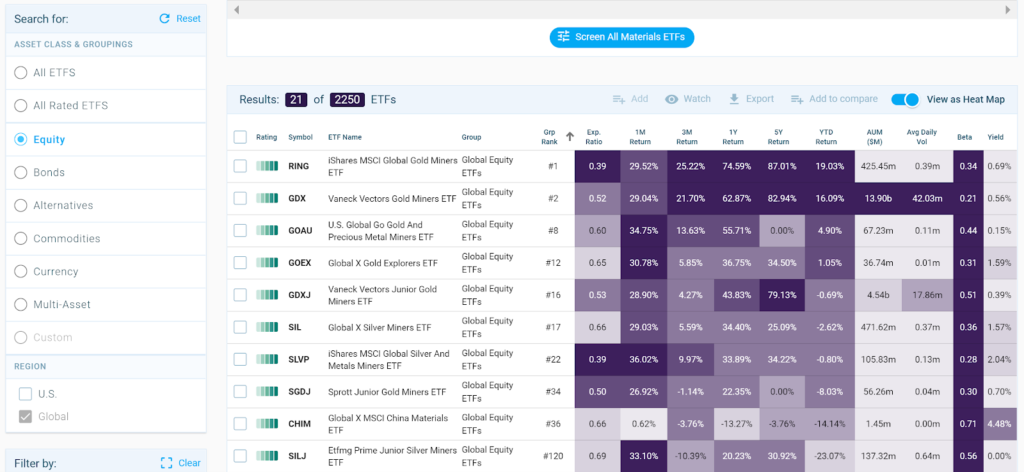

As is obvious from the chart of gold, something changed in the mid-2000’s that allowed gold to rally to new all time highs. Without going into a full dissertation about the economics of it, the gold market internals, and who the marginal buyers are, the bottom line is that US central bank money policy was very easy in the 1970’s after Nixon abandoned the Gold Standard, got tight with Paul Volker and the Fed’s decision to beat inflation in the late ‘70s and early 1980’s, and proceeded to get easy again with Greenspan in the early 2000’s. Greenspan might not have become an easy money Chairman had it not been for first the crash of ‘87 (he cut the Fed Funds rate immediately, which arguably helped the market recover) and then the “Tech Wreck” of 2000-01 when the Fed cut the fed funds rate from 6.5% to 1.75%. Eventually stock market investors started referring to the Fed’s reaction to market turmoil as “The Greenspan Put”, as easy money would bail out investors every time. Sound familiar? As we now embark on “QE infinity” and a Federal Reserve that will “do whatever it takes”, we are definitively in an easy money environment and I’m hard pressed to see anything on the horizon that will move the Fed away from that. While physical gold is hard to buy and store, and even ETFs that try to invest directly into the metal are somewhat flawed, there are some great options in gold mining ETFs. Furthermore, with low oil prices, gold mining companies will benefit as diesel fuel (and petroleum in general) are large input prices to the mining of gold. I took a look at all global material stock ETFs in our PortfolioWise platform and this is what came up:

The number one and two ranked ETFs in global equity materials ETFs are RING (the iShares MSCI Global Gold Miners ETF) and GDX (the Vaneck Vectors Gold Miners ETF). I also sorted by the Expense Ratio (not shown here), and while RING is somewhat cheaper than GDX, they both are relatively low expense ways to get diversification among global gold mining companies. The markets remain volatile and nobody knows what the economic impact of Covid-19 and our “stay at home” orders will be. We really have no idea what corporate earnings for 2020, and even 2021 will look like. There have already been several retailers that filed for bankruptcy, and unfortunately there will be other businesses that follow. It’s hard to say what spot gold will do after the recent spike higher, but for pure diversification, and the virtual certainty that the Fed will continue an easy money policy, maybe global gold miner ETFs have some merit in your client’s portfolios.