In last week’s post I wrote about the fact that following Charmain Powell’s FOMC press conference, it became clear that rates are likely going to stay lower for longer. This will have a direct impact on the fixed income portion of client portfolios, especially as it relates to the “income’ side of the equation. You can read the entire post here.

This week we are going to turn our attention to the equity side and the impact of Powell’s presser. When Powell said “We are not even thinking about, thinking about raising rates,” what I heard was “there is no / little / slow growth for the next 18 months. I hope I am wrong but I don’t think that I am. With this in mind, investors are likely to continue to pay up for “growth.” Think about it, when something is scarce, we put a premium on it (remember toilet paper in the February and March?). I say continue because I am not a believer in the growth to values shift that everyone…especially value managers have been eagerly awaiting for about a decade. Yes, value had a nice run off of the March lows in the equity market but we have seen this game before. Look no further than the fourth quarter of last year when a similar rotation began to take shape (remember when the US / China trade deal was our biggest concern) but was quickly reversed in January. In my mind, until proven otherwise, this is another instance of Lucy pulling the football away and Charlie Brown going sailing through the air!

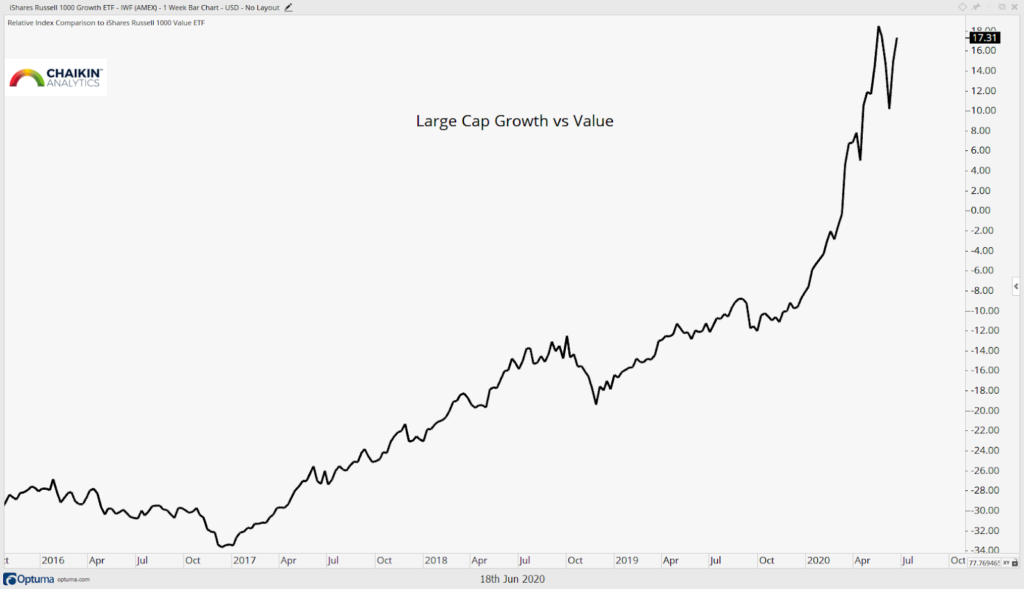

Here is the ratio of the iShares Russell 1000 Growth ETF (IWF) to the iShares Russell 1000 Value ETF (IWD)….a clear trend up and to the right signals the outperformance by “growth.”

Sliding down the market cap spectrum to the mid-caps, we can see the exact same chart (essentially). Here the ratio of the iShares Russell Mid Cap Growth ETF (IWP) to the iShares Russell Mid Cap Value ETF (IWS).

How about small caps? I think by now you know where this is going to but I am going to show you the chart of the iShares Russell 2000 Growth ETF (IWO) relative to the iShares Russell 2000 Value ETF (IWN) anyway.

And here it is as one chart. The iShares Russell 3000 Growth ETF (IUSG) vs the iShares Russell 3000 Value ETF (IUSV) ratio is in the process of making a new high. The green boxes are other times in the past five years when I have been told that “it was time for value to lead growth.”

That’s great Dan, but what about going forward? Fair question and I can give you the whole pitch about momentum and trends in motion and “the trend is your friend” but that would be a little cliche, especially coming from someone with CMT after his name. But what we can do is take a look at the ETF ratings for the six funds across the three market cap levels to get a sense for if this trend is likely to persist or if this time is different.

At each market cap level (I am not going to micro here) the growth ETF has a bullish ETF rating while the value ETF is neutral. This is very interesting especially when you consider that the ETF rating takes into account the individual ratings of the stocks that are holdings within the fund. Why? Because the Power Gauge Model that rates the stocks takes valuation into account but it seems that the growth factors are winning out. So the odds favor growth continuing to lead value. And if I’m wrong now? Then my view is that there will be plenty of time to hop on the value train. However, as I wrote earlier and expressed at 31:30 in this hit I did for Bloomberg on Wednesday, I do not think that I am wrong here!

The Chairman of the Federal Reserve just signaled that the US (and frankly global) economy is likely going to have little to no growth through the end of 2022. Do you think it is a good idea to fade that view? Would you rather be Lucy or Chuck?